The New Architecture of Money: How Digital Identity, Programmable Currency, and the Infrastructure Arms Race Are Reshaping Capital in 2026

As we enter the second quarter of 2026, the world is navigating a set of overlapping disruptions that are more structural than cyclical. The Middle East conflict and the effective closure of the Strait of Hormuz have pushed oil above USD 100 per barrel and reintroduced the spectre of stagflation across major economies. The United States has built a new legal architecture for programmable digital money through the GENIUS Act. The European Central Bank is on track to pilot a digital euro by 2027. Sam Altman's iris-scanning World ID is now integrated into Tinder, Zoom, and Docusign. And a global arms race for AI data infrastructure has redirected hundreds of billions of dollars of capital into the physical assets that will run the next phase of the global economy.

None of this is speculative. These are facts unfolding in the present tense, and together they describe something larger than any individual news cycle: a fundamental rewiring of how money works, how identity is verified, and what kind of infrastructure the modern economy is built on. For property investors, understanding that rewiring is not an academic exercise. It is the lens through which capital allocation decisions over the next decade will either make sense or fail to.

This edition covers:

The global macro backdrop in May 2026, including the Strait of Hormuz shock, oil markets, and where central banks are positioned

The redesign of money, from the GENIUS Act and programmable stablecoins to the digital euro and what it means for real assets

The emergence of identity as infrastructure, World ID, biometric systems, and the proof-of-personhood economy

The physical infrastructure arms race and why Southeast Asia is at its centre

What all three shifts mean for capital allocation, and a grounded view of both New Zealand and Malaysia within this landscape

1. The Global Backdrop: Disruption Without Direction

The defining macro event of 2026 so far is the war in the Middle East and the closure of the Strait of Hormuz. The International Energy Agency described the resulting supply disruption as the largest in the history of the global oil market. Brent crude spiked to USD 144 per barrel on 7 April before averaging USD 117 for the month. As of mid-May, WTI is trading above USD 103 per barrel and the IEA has warned that the market could remain materially undersupplied through October even if the conflict is resolved in the coming weeks. Global oil inventories drew by 129 million barrels in March and a further 117 million barrels in April. The UAE has announced its departure from OPEC, effective 1 May 2026, adding a further layer of structural uncertainty to the supply picture.

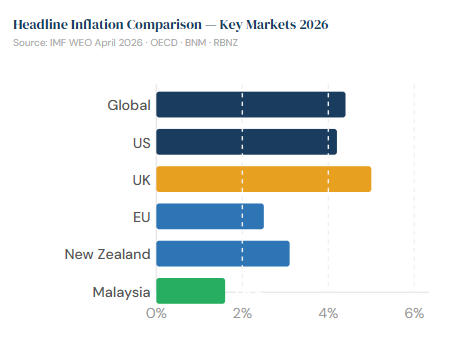

The IMF revised its global growth forecast down to 3.1% in its April 2026 World Economic Outlook, titled Global Economy in the Shadow of War, from 3.3% in January. It raised global headline inflation to 4.4%. Its adverse scenario, where the conflict extends and energy prices remain elevated, puts global growth at 2.5% and inflation at 5.4%. J.P. Morgan Global Research places a 35% probability on a US and global recession in 2026. The OECD has revised US inflation up to 4.2% for the year. UK inflation is expected to breach 5%. The European Central Bank postponed its planned rate reductions in March after Dutch TTF gas benchmarks nearly doubled to over 60 euros per MWh.

The US stock market has, somewhat counterintuitively, continued to reach record highs. Q1 2026 S&P 500 earnings growth came in at 27.8%, the strongest since Q4 2021, driven largely by Big Tech. The market appears to be making a specific bet: that central planners will choose to protect the bond market through devaluation rather than defend the currency through rate hikes, and that in a world of depreciating fiat, the nominal price of hard assets, including quality real estate, keeps rising. That is not an irrational bet. It is, however, a bet on a specific policy path, and the gap between equity markets and real economic conditions is wide enough to warrant attention.

The deeper tension is structural. The US debt-to-GDP ratio has now crossed 125%. Foreign demand for US Treasuries is declining. The Fed faces a choice that several analysts had been flagging for years: raise rates to defend the dollar and risk a bond market collapse, or cut rates to protect bonds and accept a weaker dollar and higher import inflation. The new Fed chair, to be appointed by President Trump in June 2026, adds a layer of policy uncertainty that institutional investors are already pricing into short-duration positioning.

For investors outside the US, the takeaway is that developed market macro in 2026 is not a stable anchor. It is a source of volatility. The question is not whether to take risk, but where the structural case for capital allocation is independent of that volatility.

2. The Redesign of Money: From Neutral to Programmable

For most of recorded history, money has been neutral. The currency in your account does not care what you buy with it, when you spend it, or whether you are in compliance with a government programme. That neutrality is not a technical accident. It is a foundational property of how free markets and individual autonomy have historically coexisted.

Programmable money is different in kind. It is currency with logic embedded in the instrument itself: rules about what it can buy, where it functions, when it expires, and whether it activates at all. The technology to do this at scale has existed for several years. What changed in 2025 was the institutional and legal architecture needed to deploy it.

In July 2025, the US passed the GENIUS Act, the first comprehensive federal framework for payment stablecoins. These are digital assets pegged one-to-one to the US dollar and issued on a blockchain. The Senate passed it 68 to 30. President Trump signed it the same month. The practical effects were immediate. Daily stablecoin transaction volumes rose from around one trillion dollars before the Act to four trillion dollars in the months following. The combined market cap of the two dominant stablecoins, USDC and USDT, now exceeds USD 260 billion, three times their 2023 value. In 2024, stablecoin volume already surpassed Visa and Mastercard combined. JPMorgan and Citigroup launched regulated stablecoin divisions in early 2026. Mastercard began bridging its traditional payments rail with blockchain-native digital dollars. Insurance giant Aon processed its first stablecoin premium payment in March 2026, citing the GENIUS Act's legal clarity as the deciding factor.

What the Act also did, less prominently discussed, is require all stablecoin issuers to maintain KYC, anti-money laundering compliance, and Treasury Department connectivity. Every digital dollar transaction is identifiable by design. The infrastructure for programmable money, with conditions on what it can do and who can use it, is not a future feature request. It is the legal architecture being implemented right now.

Europe is building the same capability through a different route. The ECB completed its preparation phase for the digital euro in October 2025 and moved to technical readiness. Assuming EU legislation passes in 2026, a pilot begins in mid-2027, with full issuance targeted for 2029. The ECB has publicly committed that the digital euro will not be programmable money in the restrictive sense. However, the system is being designed with conditional payments, where funds are held in escrow and released only when a specified condition is met. A group of 70 economists, including Thomas Piketty, wrote to the European Parliament in early 2026 arguing that the distinction between programmable money and programmable payments is architecturally thin. The European Parliament is set to vote on the digital euro legislation in June 2026.

The US took a different and notable path on the government-issued version. Congress passed the Anti-CBDC Surveillance State Act in July 2025, prohibiting the Federal Reserve from issuing a Central Bank Digital Currency directly. The US has effectively privatised its programmable money infrastructure through regulated stablecoins rather than creating a central bank version. The result is the same underlying architecture, just with private intermediaries between the individual and the state.

For property investors, the most direct implication is the tokenisation of real assets. Larry Fink, CEO of BlackRock, the world's largest asset manager overseeing approximately 14 trillion dollars in assets, has stated publicly that the firm plans to eventually trade all stocks and bonds as digital tokens on a single blockchain ledger. BlackRock filed new tokenisation proposals with the SEC on 8 May 2026. Total real-world assets tokenised globally reached USD 21 billion in January 2026, up 260% year on year. Deloitte projects the tokenised real estate market alone will reach nearly four trillion dollars by 2035. Dubai's government Land Department launched a blockchain property deed system in 2025, enabling fractional ownership with entry points around USD 545. The St. Regis Aspen Resort was tokenised on the SolidBlock platform. Platform RealT has tokenised over 150 homes across 40 US markets at around USD 50 per fractional share.

The investment case is straightforward: when an asset is tokenised, its valuation is reassessed by a global pool of capital with 24-hour liquidity and near-zero friction. Quality assets with clear title, strong income, and genuine scarcity are the first candidates. Being positioned in them before that revaluation process begins means entering at pre-tokenisation pricing. That window is narrowing.

3. Identity as Infrastructure: Proving You Are Human

In April 2026, a company called World, co-founded by Sam Altman of OpenAI, announced integrations with Tinder, Zoom, and Docusign. The mechanism is simple: users who visit one of World's Orb devices, a silver sphere about the size of a bowling ball deployed across major US cities, submit to an iris scan. The device converts their iris pattern into a cryptographic hash, issues a World ID credential, and permanently deletes the original image. The hash sits on a blockchain. Over 18 million people have done this voluntarily as of May 2026.

The reason these platforms want this is not abstract. Tinder reported a 45% year-on-year increase in AI-driven bot activity in 2025. Zoom recorded a 30% rise in synthetic identity fraud on enterprise accounts over the same period. Deepfakes can now pass as real people in video calls convincingly enough that fraud, deepfake impersonation, and AI-generated fake profiles have become operational business problems at scale. Proving you are a real human being has crossed from a philosophical question to an urgent commercial requirement.

Sam Altman has stated publicly that proof of human will eventually be required by every website, every app, and every transaction on the internet. That is a credible projection. The pilot launches on Tinder and Zoom in Q3 2026, with five million opt-ins projected by Q4. Early internal data shows verified users seeing engagement and trust scores rise by around 60%, creating organic adoption incentive beyond the security argument.

The concerns are substantive and worth acknowledging directly. Your iris cannot be changed the way a password can. Once that biometric data exists, even in hashed form, it can be subpoenaed, accessed under future laws that do not yet exist, or compromised in ways that current privacy policies cannot anticipate. Brazil, Germany, South Korea, and Kenya have all launched investigations or enacted restrictions on the programme. These are not fringe objections. They are serious governance questions that remain unresolved.

What is not in question is that the identity infrastructure being built, through World ID, airport biometrics at Singapore Changi and major UAE hubs, national digital ID programmes, and the Bank of International Settlements documentation that digital IDs and central bank digital currencies are designed to be interoperable, represents a structural shift in how people and capital interact with every kind of institution. The system being built is one where identity is a portable credential, verified by biology rather than a document, and attached to financial access rather than held separately from it.

China provides the most complete real-world illustration of what this architecture looks like once in place. In March 2025, the Chinese government updated its Social Credit System with 23 new measures, including industry-specific blacklists covering real estate, internet services, energy, and finance. Businesses classified as seriously dishonest face bans on government procurement, tax incentives, and capital markets access. As of September 2025, approximately 200,000 individuals were added to blacklists in 2025 alone, 46% for contractual disputes. The system remains fragmented rather than unified, and the corporate compliance layer is far more developed than the individual scoring side. But the infrastructure for integration is advancing with each policy update, and the direction is clear.

For investors, the practical implication is twofold. First, jurisdictions with strong rule of law and constitutional protections around financial privacy become structurally more attractive as destinations for capital. Second, the physical infrastructure required to run identity verification and programmable money systems at global scale needs to live somewhere. That somewhere is, in Southeast Asia, increasingly Malaysia.

4. The Infrastructure Arms Race: Where the Physical Build Is Landing

The data centre buildout underway globally right now is unlike anything the property industry has seen before in terms of capital velocity and geographic concentration. In the first half of the 2026 US financial year alone, the Department of Defense committed over USD 32 billion in contract ceiling to AI, cloud computing, cybersecurity, and data analytics. The Pentagon awarded USD 200 million each to xAI, OpenAI, Google, and Anthropic in a single round to develop autonomous AI systems capable of operating in classified environments. Palantir, which provides data integration and predictive analytics to governments, intelligence agencies, and militaries worldwide, secured a USD 10 billion, ten-year US Army contract in August 2025. The company now forecasts 2026 revenue of USD 7.18 to 7.20 billion, a 60% increase from 2025, with US government revenue growing 66% in a single quarter.

The commercial side is equally significant. In Southeast Asia alone, data centre investment reached USD 3.2 billion in 2024, roughly four times the prior year, accounting for approximately 40% of total industrial sales volume across the region. Malaysia, Singapore, and Indonesia led the buildout, with Malaysia standing out for its combination of competitive power costs, government-aligned digital infrastructure policy, and proximity to Singapore's land-constrained market.

Hyperscale operators including Microsoft, AWS, and Google Cloud have been securing large industrial land parcels across Johor's key corridors. The Johor-Singapore Special Economic Zone, formally established in January 2026, adds a policy layer that further concentrates demand in a geography already under supply pressure. Johor recorded approximately RM 91 billion in approved investments in 2025 alone. Industrial vacancy rates in the corridor are tightening not because sentiment is improving but because the space is genuinely being occupied.

The manufacturing dimension compounds this. Between 2018 and 2024, approximately 45% of Chinese offshore manufacturing foreign direct investment was directed toward ASEAN economies. Malaysia's semiconductor clusters have seen meaningful capacity expansions as global firms diversify production away from single-country dependency. The China Plus One reallocation and the data centre boom are generating dual demand for industrial land in the same corridors, creating a structural floor under both rents and valuations.

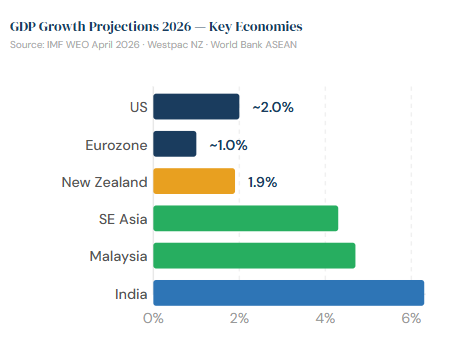

Whether your interpretation of this buildout is optimistic, that AI productivity gains will be enormous and the infrastructure is simply what that requires, or more cautious, that the scale of data required to run identity systems, programmable money, and population-level analytics demands exactly this physical footprint, the investment conclusion is the same. The infrastructure is being built. It needs land, power, cooling, and logistics networks. The markets best positioned to absorb that demand are those with the right cost structures, government alignment, and existing supply chain depth. On all three criteria, Malaysia scores well. On macroeconomic stability, with GDP growth projections of 4 to 5%, inflation at approximately 1.6%, and the OPR steady at 2.75%, it adds a fourth.

5. New Zealand and Malaysia: An Honest Assessment

New Zealand is navigating a period of genuine difficulty, and we think it is more useful to address that directly than to frame it otherwise.

National property values fell 1.0% over 2025, with the median now sitting approximately 17.6% below the November 2021 peak. Wellington is down 25.9% from its peak. Auckland is down 21.8%. Nearly 20% of Auckland sellers who transacted in Q1 2026 did so at a loss, rising to over 40% for apartment vendors. Net migration to the year ending November 2025 came in at 10,681, down 92% from 2023 levels, removing one of the primary structural demand drivers for residential property. The Middle East conflict has added a further layer of headwinds: Westpac revised its 2026 New Zealand GDP forecast down to 1.9% in March, projecting a quarterly GDP contraction in the June quarter. ANZ economists are forecasting a 2% decline in house prices for the full year. The RBNZ's path toward further OCR easing has stalled as wholesale swap rates have risen in response to oil-driven inflation expectations.

The honest read is that the macro backdrop in New Zealand is not positioned to generate the kind of capital appreciation story that attracted investors over the previous decade. The structural drivers that supported that story, population growth, cheap credit, supply constraints, have either reversed or weakened. The market that remains is an income market, where returns come from yield rather than revaluation.

Within that framework, there are genuine pockets of opportunity. Industrial assets in South Auckland and Christchurch where vacancy rates remain below 3% continue to perform on fundamentals independent of sentiment. Healthcare and essential services facilities with long lease structures and non-discretionary tenant demand are showing resilience across the cycle. Regional commercial assets at yields above 8% in markets with constrained new supply represent defensible income positions. The framework for New Zealand in the second half of 2026 is income first, selectivity as the primary risk tool, and a realistic time horizon for capital appreciation that extends further than it did three years ago.

Malaysia operates from a different position. GDP growth projections of 4 to 5% for 2026, inflation contained at approximately 1.6%, a stable OPR at 2.75%, and the structural demand tailwinds described in this edition, data centres, manufacturing relocation, the Johor-Singapore SEZ, all point to a market where fundamentals are generating demand without needing sentiment to cooperate. Malaysia ranked 23rd globally in the Milken Institute's 2026 Global Opportunity Index, first in Southeast Asia, with high scores in financial services and institutional strength. CBRE forecasts a 5 to 10% year-on-year increase in Asia Pacific commercial real estate investment volumes in 2026, following a 22% rebound in 2025.

The real yield available on Malaysian industrial assets, at 7 to 8% nominal with inflation below 2%, represents a spread that developed markets are structurally unable to replicate. For cross-border investors, the ringgit's stabilisation after a prolonged period of weakness removes a key currency risk layer and allows analysis to focus on asset fundamentals rather than defensive positioning.

The divergence between these two markets is not a temporary cycle difference. It reflects the underlying question this edition has been asking throughout: which markets are adjacent to the infrastructure being built for the next phase of the global economy, and which are working through the accumulated weight of the last one. That is not a criticism of New Zealand, and it is not an uncritical endorsement of Malaysia. It is the structural read we are working from as we approach capital allocation in the second half of 2026.

6. Featured Listings: Strategic Entry Points

While many investors remain on the sidelines awaiting clearer signals, underlying fundamentals across selected segments have already begun to stabilise. In this phase of the cycle, opportunities are less about broad market timing and more about identifying assets where income, demand, and supply dynamics are already aligned.

New Zealand

Auckland — Fully Leased Mixed-Use Retail Investment

Property Type: Retail / Hospitality, Mixed-Use

Estimated Value: ~NZD 3.5 million

Estimated Yield: ~5.5%

Floor Area: ~313 sqm

Tenancy: 2 tenancies, 100% occupied

Notes:

A fully leased ground-floor retail and showroom asset within a recently completed, award-winning mixed-use development in the Auckland city fringe. The property occupies a prominent corner position within a high-density residential precinct, anchored by an established all-day hospitality operator on a 6-year lease with fixed annual rental increases and multiple renewal rights. A secondary tenancy adds diversified income across showroom and professional office use. The building is finished to a high standard with over four metres of stud height and significant natural light frontage.

Investment Potential:

The Auckland city fringe mixed-use corridor is one of the most structurally resilient segments of the NZ commercial market, supported by high residential density, consistent pedestrian demand, and the non-discretionary nature of neighbourhood hospitality and professional services. In a market where broad commercial sentiment remains cautious, a fully leased asset anchored by an established operator with a long lease and fixed escalations provides exactly the income visibility that the current cycle rewards. The property is not dependent on market recovery to perform. It is generating income today, at a yield level that reflects current pricing without requiring a rate cut to justify entry.

Auckland (South) — Cold Storage and Logistics Facility

Property Type: Industrial / Cold Storage and Distribution

Estimated Value: ~NZD 60 million

Estimated Yield: ~7.5%

Land Area: ~46,000 sqm (Freehold)

Building Area: ~16,000 sqm

Site Coverage: ~34% (significant development optionality)

Notes:

A significant chilled and frozen distribution facility in Auckland's most established southern industrial precinct, offering exceptional connectivity to the motorway network, Auckland Airport, and the Port of Auckland. The asset is currently leased to a major national grocery operator, providing secure income in the near term. The large freehold site with low site coverage creates meaningful optionality for future expansion or staged redevelopment alongside the existing income stream.

Investment Potential:

Cold storage infrastructure in New Zealand is among the most structurally undersupplied segments of the industrial market. The cost and complexity of replicating a facility of this scale and specification from scratch creates a durable floor under existing asset values, regardless of broader sentiment conditions. The near-term lease expiry is not a risk but an active opportunity: the ability to reset to current market rents in a precinct where cold chain vacancy is effectively zero, or to reposition for a new long-term operator at a substantially improved rental base. For investors operating within the income-first framework appropriate to the current NZ cycle, this asset represents a rare combination of covenant-grade income today and material value-add optionality on a short horizon. The freehold land holding at this scale, in this location, is a finite asset that does not come to market often.

Malaysia

Shah Alam, Selangor — Data Centre Ready Industrial Facility

Property Type: Detached Industrial / High Power Infrastructure

Estimated Value: ~RM 38M

Estimated Yield: ~7.5%

Land Area: ~65,000 sqft

Floor Area: ~48,000 sqft

Power Supply: ~2,000 Amp / TNB substation on title

Notes:

A recently upgraded industrial facility in Shah Alam's Section 26 industrial zone, configured for high-power operational tenants including light data infrastructure, semiconductor assembly, and precision manufacturing. The facility sits within 2km of three active data centre campuses and directly adjacent to an established logistics corridor serving Port Klang.

Investment Potential:

Investment Potential: Shah Alam is emerging as the overflow corridor for Klang Valley's data centre demand, as Cyberjaya and Subang have limited remaining land at viable costs. The 2,000 amp power supply on title, rare in the sub-RM 50M industrial segment, makes this asset immediately attractive to a tenant pool that would otherwise require 18-plus months of infrastructure lead time. This ties directly to the article's infrastructure thesis: owning high-power industrial stock before hyperscale operators exhaust the primary corridors means entering ahead of the repricing.

Johor Bahru (Kulai) — Logistics Hub, Freehold Industrial

Property Type: Single-Tenanted Logistics Warehouse

Estimated Value: ~RM 28M

Estimated Yield: ~7.8%

Land Area: ~120,000 sqft

Floor Area: ~85,000 sqft

Tenure: Freehold

Notes:

A large-format freehold logistics warehouse in Kulai, 30km north of Johor Bahru city and directly accessible from the North-South Expressway. Currently tenanted to a regional e-commerce fulfilment operator on a 5-year lease with a rental escalation clause. Ceiling height of 10 metres, 6 loading docks, and a full truck yard.

Investment Potential:

Kulai is one of the Johor corridor's most active logistics zones due to its midpoint position between JB Port and Kuala Lumpur's distribution network, and its positioning just outside the premium land pricing of the SiLC and Nusajaya zones. The freehold title, large format, and 5-year lease to a logistics operator tied to Southeast Asia's e-commerce growth provide exactly the income visibility and exit liquidity profile described in the article. As the Johor-Singapore SEZ drives further manufacturing and trade activity northward along the corridor, Kulai assets are structurally well placed to absorb tenant overflow from tighter southern markets.

Want to discuss any of these opportunities further? Reach out to our team directly:

Contact Information :

Petrus Yen - Managing Director

Petrus@fairhavenproperty.co.nz

Daarshan Kunasegaran

Daarshan.Kunasegaran@fairhavenproperty.co.nz

Disclaimer:

The property details, financial figures, and projections provided in this article are based on publicly available information and internal estimates. They are intended for informational purposes only and do not constitute financial advice or an offer to invest. Projections such as IRR and equity multiples are indicative only and subject to change based on market conditions, financing terms, and execution strategy. Interested parties should conduct independent due diligence and consult with a qualified advisor before making any investment decisions. Fairhaven Property Group accepts no liability for decisions made based on the information presented herein.