As of March 2026, oil has briefly surged above $100 as geopolitical tensions escalated across key energy-producing regions. Financial sanctions continue to reshape global trade relationships. Central banks are quietly diversifying reserves. Digital settlement networks are expanding. Major banks are experimenting with tokenised bonds and programmable financial infrastructure.

Individually, none of these developments are revolutionary.

Collectively, they point to something more significant.

The global financial system is gradually evolving as geopolitical power, energy markets, and financial technology converge.

For decades, the international monetary system has been anchored by the petrodollar framework, where energy markets, global trade, and financial infrastructure reinforced demand for the U.S. dollar. But as financial sanctions expand and digital financial infrastructure develops, countries and institutions are beginning to explore alternative settlement mechanisms.

This does not necessarily signal the end of the current system. Rather, it suggests the early stages of an adjustment in how global capital moves, settles, and interacts with real assets.

For investors, periods of financial transition rarely begin with dramatic crises. They begin with subtle changes in infrastructure, incentives, and capital flows.

This month’s report examines how those changes are unfolding.

This edition covers:

The historical relationship between conflict and the evolution of monetary systems

How the petrodollar framework shaped modern global finance

The growing use of financial sanctions and the fragmentation of financial infrastructure

Why tokenisation and programmable finance may reshape settlement systems

The continued strategic role of energy markets in global monetary dynamics

What these developments may mean for investors allocating capital into real assets

The property outlook in New Zealand and Malaysia within this evolving financial environment

1.Conflict and the Evolution of Monetary Systems

Periods of geopolitical tension have historically played a decisive role in reshaping the global financial system. While monetary frameworks often appear stable for long stretches of time, many of the most significant shifts in financial architecture have occurred during moments of conflict, economic stress, or structural transition. The Bretton Woods system that defined post-war finance emerged from the aftermath of World War II, while the collapse of the gold standard in the early 1970s gave rise to the modern dollar-based system that continues to underpin global trade today.

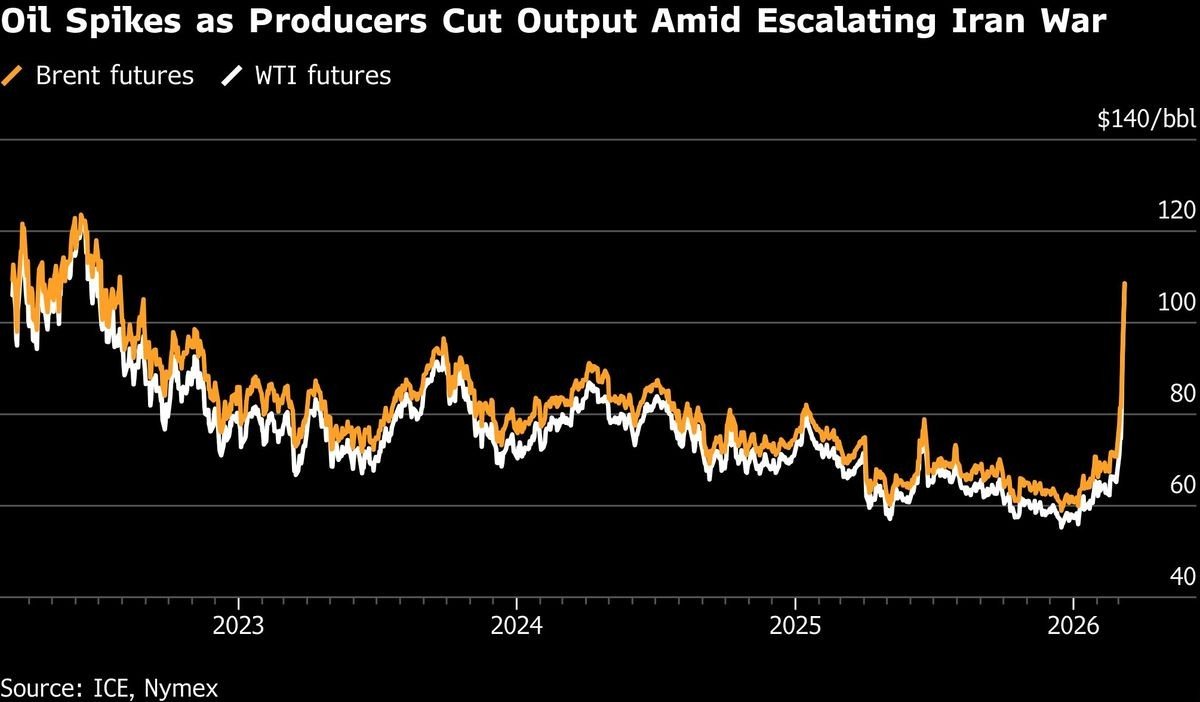

Recent developments suggest the world may be entering another period of systemic adjustment. Heightened geopolitical tensions, including the recent escalation involving Iran, have once again brought energy markets, financial sanctions, and international payment systems into sharp focus. Conflicts in strategically important regions often extend beyond military considerations; they also influence how resources are priced, how trade is settled, and ultimately how financial power is distributed across the global economy.

Recent volatility in global oil markets illustrates how quickly geopolitical events can influence the broader economic landscape. Following escalating tensions in the Middle East, crude oil prices surged sharply, with Brent crude briefly moving above $100 per barrel as markets reacted to potential disruptions in supply and regional instability.

Sharp movements in energy prices often serve as an early signal of wider economic and financial implications. Because oil remains one of the most globally traded commodities, fluctuations in its price can influence inflation expectations, trade balances, and capital flows across multiple economies.

At the same time, the increasing use of financial sanctions and restrictions on international payment networks has highlighted the degree to which modern finance is intertwined with geopolitical influence. Access to the global banking system, reserve currencies, and payment infrastructure has become an increasingly important strategic consideration for many nations. As a result, governments and financial institutions alike have begun exploring alternative mechanisms for settling trade, moving capital, and maintaining financial sovereignty.

Overlaying these geopolitical dynamics is a parallel technological shift within the financial system itself. Advances in digital infrastructure, including the tokenisation of financial assets and the development of new settlement networks, are beginning to change how money and assets can move across borders. While still in relatively early stages, these developments suggest that the financial architecture supporting global trade may be gradually evolving.

Taken together, the convergence of geopolitical tension, energy market volatility, and technological innovation raises an important question for investors and policymakers alike: whether the current financial system is approaching another phase of structural change, and what form the next iteration of global financial infrastructure may take.

2. The Current System:The Petrodollar Framework

The End of Bretton Woods

The foundations of the modern global financial system were established in the early 1970s following the collapse of the Bretton Woods monetary framework. Under Bretton Woods, the U.S. dollar was convertible into gold, providing a stable anchor for international currencies. However, growing fiscal pressures and increasing global demand for dollars eventually made the system unsustainable. In 1971, the United States formally ended the dollar’s convertibility into gold, effectively bringing the Bretton Woods system to a close.

With the removal of the gold backing, the international monetary system required a new mechanism to sustain global demand for the U.S. dollar. This transition marked the beginning of what would later become known as the petrodollar system.

Energy Markets and Dollar Demand

In the years that followed, a series of agreements between the United States and major oil-producing nations led to the widespread adoption of the U.S. dollar as the primary currency for global oil transactions. Since oil is one of the most critical commodities in the global economy, this arrangement created a powerful and self-reinforcing cycle of dollar demand.

Countries seeking to import energy were required to maintain dollar reserves, while oil-exporting nations accumulated large volumes of dollar-denominated revenue. These revenues were often reinvested into U.S. financial assets, particularly government bonds, further reinforcing the central role of the dollar within the global financial system.

The Foundation of Modern Dollar Dominance

Over time, the linkage between energy markets and the U.S. dollar became a cornerstone of international finance. The widespread use of the dollar in commodity markets, global trade, and financial transactions helped solidify its position as the world’s primary reserve currency.

This structure provided the United States with several structural advantages. Persistent global demand for dollar liquidity supported deep and highly liquid capital markets, while foreign purchases of U.S. debt helped finance fiscal deficits. For many countries, holding dollar reserves became a practical necessity for participating in global trade and maintaining financial stability.

While the petrodollar system has remained remarkably resilient for decades, its stability ultimately depends on a combination of geopolitical relationships, energy market dynamics, and the broader infrastructure that underpins international finance.

3. Financial Weaponisation and the Fragmentation of Global Finance

Sanctions as a Strategic Tool

In recent years, financial systems have increasingly become instruments of geopolitical influence. Economic sanctions, restrictions on financial institutions, and limitations on access to international payment networks have emerged as powerful tools used by governments to exert pressure without direct military confrontation. By restricting access to the global financial system, countries can significantly limit a nation’s ability to conduct international trade, access foreign capital, or stabilise its currency.

One of the most visible examples occurred following the invasion of Ukraine in 2022, when a significant portion of Russia’s foreign currency reserves held in Western jurisdictions was frozen. The move demonstrated the extent to which reserve assets, long considered neutral financial buffers, could become subject to geopolitical leverage. For many countries observing these developments, the episode served as a reminder that access to global financial infrastructure is not purely economic, but also political.

Dependence on Financial Infrastructure

Modern international finance relies heavily on interconnected systems that facilitate cross-border payments and trade settlement. Networks such as SWIFT, correspondent banking relationships, and global clearing systems form the backbone of this infrastructure. While these systems have enabled decades of efficient globalisation, they also concentrate considerable influence within a relatively small number of financial institutions and jurisdictions.

When access to these networks is restricted, the consequences can be immediate and far-reaching. Financial institutions may find themselves unable to settle transactions, international trade can become more complex, and capital flows may be disrupted. As a result, the structure of financial infrastructure itself has become an important strategic consideration for many governments.

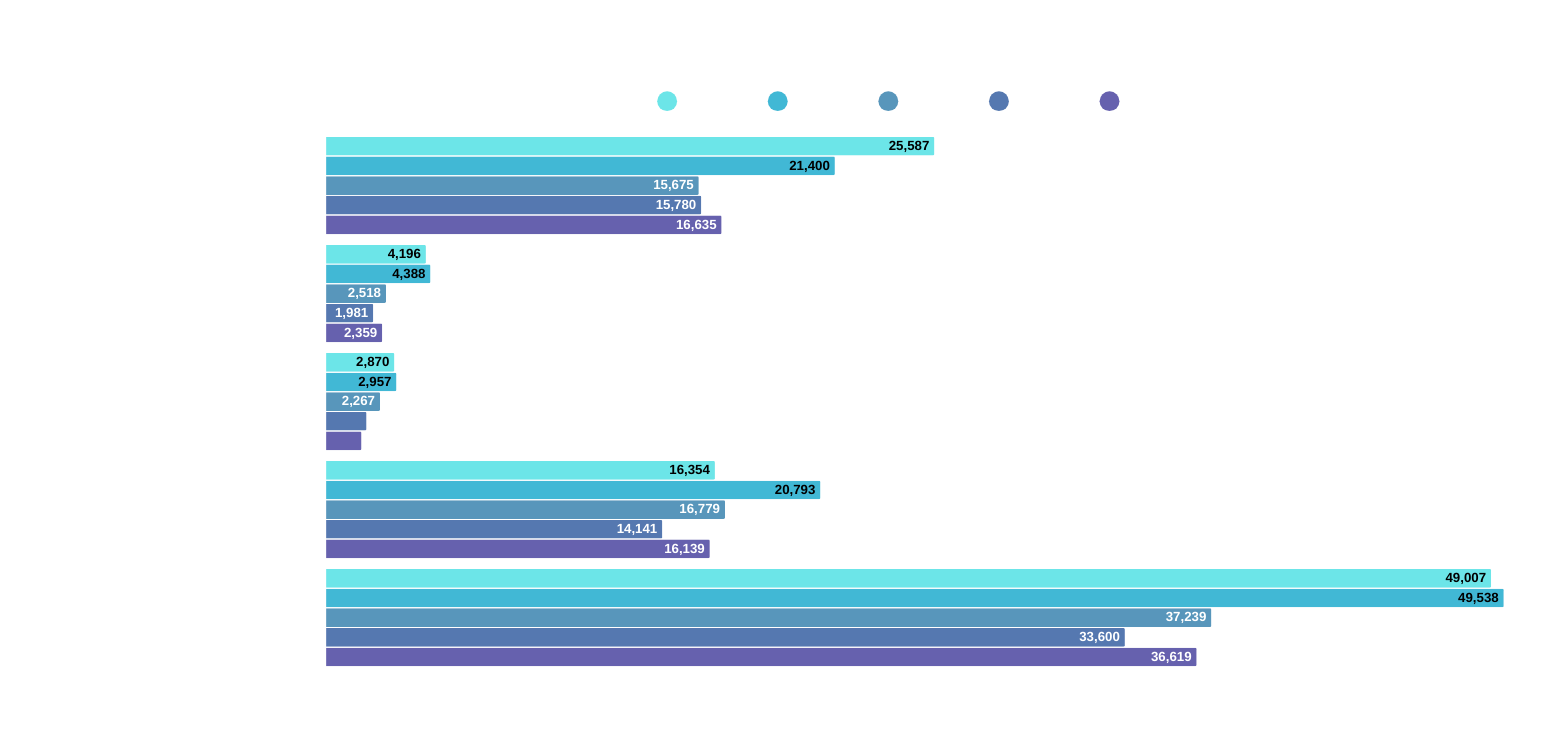

The Dollar’s Dominance and Gradual Diversification

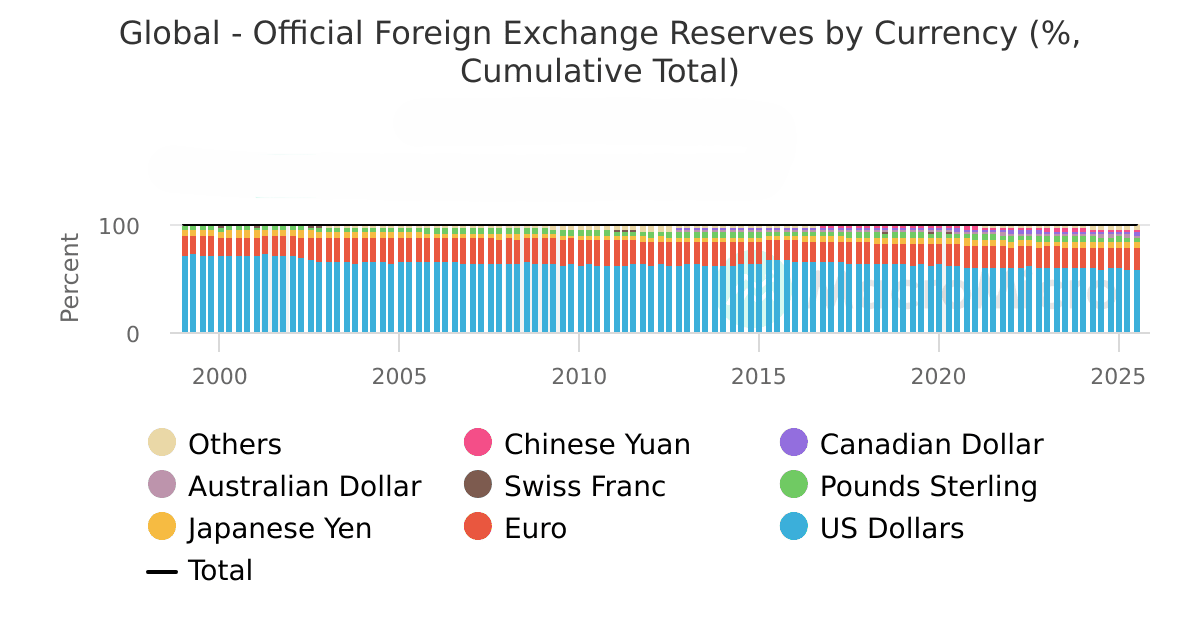

Despite increasing geopolitical tensions and discussions around alternative financial systems, the U.S. dollar continues to dominate the global monetary system. Central banks around the world still hold the majority of their foreign exchange reserves in dollar-denominated assets, reflecting the depth, liquidity, and stability of U.S. financial markets.

However, recent years have also seen a gradual diversification of reserve holdings. Other currencies such as the euro, Chinese yuan, and Japanese yen have slowly increased their presence within global reserve portfolios, reflecting the evolving dynamics of global trade and financial relationships.

The chart above illustrates how the composition of global reserves has evolved over time. While the U.S. dollar remains the dominant reserve currency, its share has gradually declined from earlier peaks as central banks diversify their holdings across a broader range of currencies.

Growing Interest in Alternative Settlement Systems

In response to these developments, a growing number of countries have begun exploring ways to reduce their dependence on a single financial architecture. Efforts to develop alternative payment networks, bilateral trade settlement arrangements, and regional financial systems have gradually gained momentum.

These initiatives do not necessarily signal an immediate departure from the dollar-based system. Rather, they reflect an increasing desire among some nations to diversify their financial options and reduce vulnerability to external financial pressure.

As geopolitical tensions persist and the global economic landscape becomes more multipolar, the search for alternative financial infrastructure is likely to continue. At the same time, technological developments are beginning to offer new possibilities for how financial assets and transactions can be structured in the future.

4. Tokenisation and the Emergence of New Financial Infrastructure

What Tokenisation Means

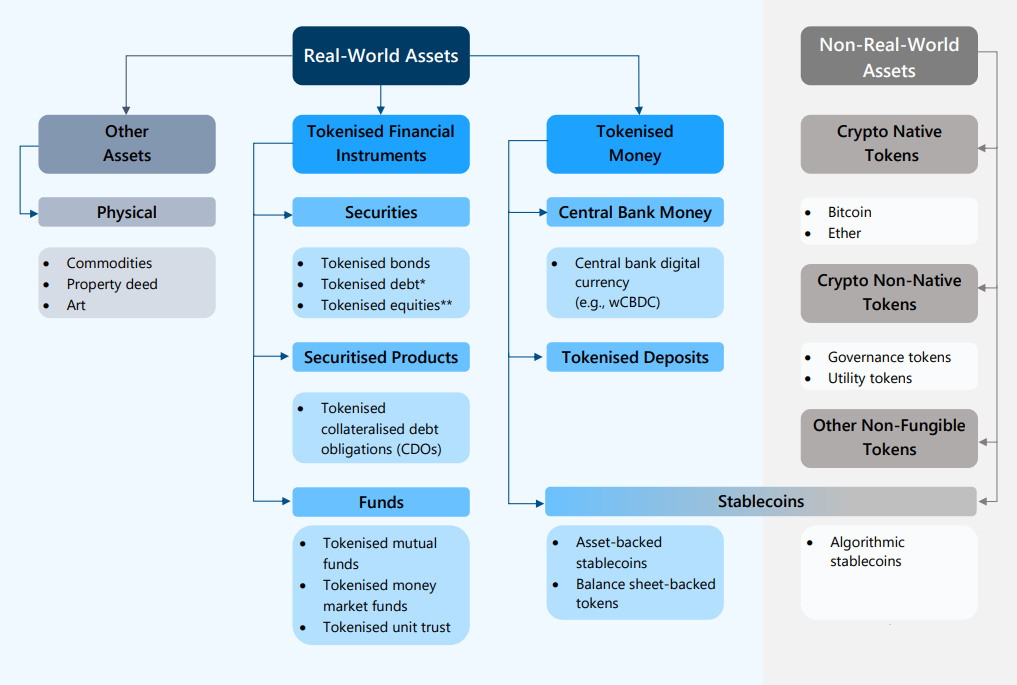

Amid these geopolitical shifts, technological innovation is beginning to reshape the underlying infrastructure of financial markets. One of the most significant developments in recent years has been the concept of tokenisation, which refers to the process of representing real-world assets as digital units on programmable ledgers.

In practical terms, tokenisation allows assets such as government bonds, commodities, equities, or real estate to be recorded and transferred digitally through blockchain-based systems or other distributed ledger technologies. Rather than relying on multiple intermediaries to verify and settle transactions, ownership can be recorded directly on a shared digital ledger.

While the concept is still evolving, many financial institutions are increasingly exploring tokenisation as a way to modernise the way financial assets are issued, traded, and settled.

Applications Across Financial Markets

The potential applications of tokenisation extend across a wide range of asset classes. Governments and financial institutions have begun experimenting with tokenised bonds and treasury securities, allowing investors to access traditionally large institutional markets through smaller, digitally tradable units. In parallel, stablecoins backed by fiat currencies or government debt have emerged as another example of how traditional financial assets can be integrated into digital settlement systems.

Beyond sovereign debt markets, tokenisation is also being explored in commodity markets and property investments. Commodities such as gold or oil can theoretically be represented as digital tokens that correspond to physical assets, while real estate ownership can be divided into fractional digital units that may improve accessibility for investors.

Although many of these applications remain in early stages, they illustrate how tokenisation could eventually expand the ways in which assets are issued, traded, and held globally.

Modernising Financial Settlement

One of the most frequently cited advantages of tokenisation lies in the potential to modernise financial settlement systems. Traditional financial transactions often require multiple intermediaries, including clearing houses, custodians, and correspondent banks, which can introduce delays and increase costs.

Tokenised systems may allow transactions to settle more quickly, sometimes within minutes rather than days, while reducing the need for complex reconciliation between financial institutions. In addition, programmable ledgers may allow financial contracts to incorporate automated rules governing ownership transfers, payments, or compliance requirements.

These improvements in efficiency are one reason why many large financial institutions, asset managers, and central banks have begun experimenting with tokenisation frameworks.

Tokenisation as Financial Infrastructure

Importantly, the growing interest in tokenisation reflects a broader shift in financial infrastructure rather than simply the speculative aspects often associated with cryptocurrencies. While early blockchain development was closely linked with digital asset speculation, institutional interest today is increasingly focused on how distributed ledger technologies can support existing financial markets.

Major banks, asset managers, and even central banks are exploring how tokenised assets might improve settlement efficiency, expand investor access, and streamline cross-border financial transactions.

Taken together, these developments suggest that tokenisation may gradually become part of the technological foundation supporting the next phase of global financial infrastructure.

5. The Rise of Programmable Finance

From Digital Assets to Programmable Systems

As tokenisation develops, the financial system may gradually evolve toward what is often described as programmable finance . In this framework, money and financial assets are not only digitised but also embedded with rules that determine how they can be transferred, settled, or used within financial markets.

Programmable finance builds on tokenisation by allowing financial transactions to incorporate automated conditions directly within the asset itself. For example, payments could be triggered automatically once contractual conditions are met, or regulatory compliance checks could be embedded within transaction protocols. In effect, financial instruments may increasingly function as self-executing digital contracts operating on shared ledger infrastructure.

Early Developments in Tokenised Financial Markets

While still in early stages, several developments already illustrate how programmable financial systems may evolve. One example is the growing issuance of tokenised government bonds and treasury securities , which allow digital units of traditional financial instruments to be traded and settled more efficiently. These initiatives have been explored by both financial institutions and governments seeking to improve market accessibility and settlement speed.

Another rapidly expanding area involves stablecoins , which are digital tokens backed by fiat currencies or short-term government securities. Because many stablecoins are supported by holdings of U.S. Treasury assets, they effectively represent a digital extension of existing dollar-based financial markets. As stablecoin usage expands within global payment networks, they may gradually form part of the infrastructure through which digital financial transactions occur.

Central banks have also begun exploring Central Bank Digital Currencies (CBDCs) , which aim to provide official digital versions of sovereign currencies. Although the development and adoption of CBDCs vary across jurisdictions, these initiatives highlight the broader interest in modernising national payment systems.

An Evolution of the Dollar System

Taken together, these developments suggest that the next phase of the global financial system may not involve a sudden replacement of the dollar, but rather an evolution in how the dollar circulates within financial markets . Digital tokens backed by traditional financial assets, particularly U.S. government debt, may become increasingly integrated into payment systems and financial settlement networks.

In such an environment, financial assets may become more liquid, transactions may settle more rapidly, and cross-border financial flows could operate through new technological rails that complement existing banking systems. Rather than dismantling the current financial architecture, programmable finance may gradually reshape it.

As these systems develop, the intersection between technological infrastructure and geopolitical strategy is likely to become increasingly important, particularly in sectors where global trade and strategic resources play a central role.

6. Energy, Conflict, and Control of Financial Infrastructure

Energy Markets Remain the Strategic Core

Despite the rapid development of new financial technologies, the global monetary system continues to be deeply connected to energy markets. Commodities such as oil and natural gas remain fundamental to industrial production, transportation, and global trade. As a result, the mechanisms through which energy is priced and settled continue to play a significant role in shaping international financial flows.

The dominance of the U.S. dollar in global energy markets has been one of the key pillars supporting the current monetary framework. Because many energy transactions are denominated in dollars, countries involved in global trade often maintain dollar reserves to facilitate these transactions. This structure reinforces the central role of the dollar not only in commodity markets but also across broader financial markets.

Geopolitical Tensions and Strategic Resources

Conflicts involving energy-producing regions can therefore have consequences that extend beyond immediate supply concerns. Tensions in regions such as the Middle East, including the recent escalation involving Iran, often bring renewed attention to the strategic importance of energy infrastructure, shipping routes, and commodity pricing mechanisms.

In addition to physical supply risks, geopolitical tensions may also influence the financial systems through which these resources are traded. Sanctions, trade restrictions, and financial controls can affect how commodities move across borders and how payments are settled between countries.

These dynamics highlight the broader relationship between geopolitical power, energy security, and financial infrastructure.

Competition Over Financial Architecture

As geopolitical competition evolves, financial infrastructure itself is increasingly becoming an area of strategic importance. Nations and financial institutions are exploring ways to strengthen their influence over payment systems, capital markets, and settlement networks.

The development of tokenised financial instruments, digital settlement platforms, and alternative payment systems can be viewed within this broader context. While these technologies may improve efficiency and accessibility within financial markets, they also have the potential to reshape how financial power is distributed across the global economy.

Ultimately, the future financial system is likely to be shaped by a combination of technological innovation, geopolitical realities, and the continued importance of energy markets in global trade.

7. What this means for Investors

Structural Transitions in the Financial System

Taken together, the developments discussed above suggest that the global financial system may be entering another period of gradual structural transition. Geopolitical tensions, the increasing use of financial sanctions, and the emergence of new financial technologies are all influencing how capital moves across borders and how international trade may be settled in the future.

While the current dollar-based system remains deeply embedded within global markets, technological innovations such as tokenisation and programmable finance indicate that the underlying infrastructure supporting financial transactions may continue to evolve. Rather than representing a sudden break from the existing system, these developments may reflect a gradual shift in how financial assets are issued, transferred, and settled.

Periods of monetary transition are not uncommon in financial history. Changes in monetary frameworks have often occurred alongside geopolitical realignments, technological innovation, and shifts in global trade dynamics. In such environments, investors often reassess how financial infrastructure may evolve and how capital may be allocated in the future.

Investor Behaviour During Systemic Change

For investors, periods of financial transition often introduce both uncertainty and opportunity. As financial systems evolve and geopolitical dynamics shift, capital tends to reassess where long-term value and stability can be found.

Historically, assets that possess intrinsic economic value or generate consistent income streams have tended to attract greater investor attention during such transitions. Real assets, including property, infrastructure, and commodities, can provide tangible value and income generation that is less dependent on the structure of financial infrastructure itself.

While financial systems may evolve over time, the underlying economic drivers of housing demand, urban development, and population growth tend to remain more stable. These structural drivers often support long-term demand for income-generating property assets across many markets.

Digital Infrastructure and Access to Real Assets

At the same time, emerging financial technologies may gradually expand how investors access these real assets. Early developments in tokenisation suggest that digital financial infrastructure could eventually broaden access to traditionally illiquid asset classes such as property.

Although many tokenised investment models remain in early stages of development, the broader direction of travel points toward greater integration between digital financial systems and real-world assets. In such an environment, assets characterised by stable income streams and transparent underlying value may become increasingly relevant as financial markets evolve.

For investors, this dynamic reinforces the importance of focusing on assets supported by durable economic fundamentals. While financial infrastructure may change, the demand for housing, urban development, and income-generating property remains closely tied to real economic activity.

A Bridge Toward Property Markets

In this context, examining regional property markets provides a useful perspective on how broader macroeconomic developments may translate into tangible investment opportunities. Markets supported by strong demographic demand, stable legal frameworks, and consistent rental activity can continue to play an important role in long-term investment portfolios.

With this in mind, it is useful to examine the current conditions shaping property markets in both New Zealand and Malaysia, where structural demand drivers and economic fundamentals continue to influence the outlook for real estate investment.

8. New Zealand and Malaysia

Real Asset Markets in a Changing Financial Architecture

After examining the broader shifts occurring across the global financial system, from geopolitical tension and energy market volatility to the gradual evolution of digital financial infrastructure, the practical question for investors becomes straightforward.

Where can capital find stability, income visibility, and structural demand in an environment where monetary frameworks may be evolving?

During transitional cycles, capital typically gravitates toward jurisdictions where several key conditions align:

• policy credibility

• transparent legal frameworks

• sustainable economic demand

• income-generating real assets

In this context, both New Zealand and Malaysia continue to present compelling characteristics, though through different economic channels.

New Zealand: Stabilisation, Currency Positioning, and the Next Supply Cycle

While much of the global macro discussion focuses on financial system shifts and technological developments, real asset markets ultimately respond to a simpler set of drivers: monetary conditions, currency dynamics, and supply constraints.

In New Zealand, these three variables are now beginning to align in ways that historically precede property market stabilisation.

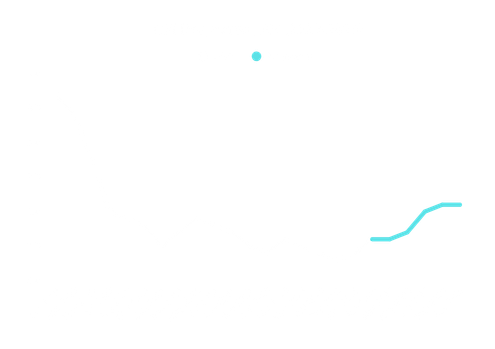

Monetary Conditions Are Normalising

The first structural shift is monetary policy.

Following the aggressive tightening cycle that pushed the Official Cash Rate to 5.5 percent during 2023 and early 2024 , inflation has gradually moderated toward the Reserve Bank of New Zealand’s target range.

As price pressures eased, the RBNZ began lowering rates through 2024 and 2025, bringing the OCR down to 2.25 percent by late 2025 , where it currently remains.

The chart above illustrates how monetary policy moved from restrictive to neutral conditions as inflation fell. CPI has declined sharply from post-pandemic highs, allowing the central bank to reduce borrowing costs without risking a resurgence of inflation.

For property markets, the importance of this shift is not the rate cuts themselves but the end of policy uncertainty . Property cycles rarely stabilise while interest rates are still rising. Stability tends to emerge once borrowing conditions become predictable again.

With the OCR now near estimated neutral levels, financial conditions are materially less restrictive than during the peak tightening phase.

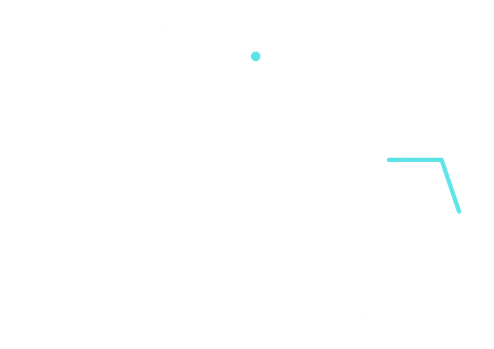

Currency Positioning Remains Supportive

Currency dynamics also play an important role in international investment decisions.

The New Zealand dollar remains below its long-term average against the U.S. dollar, even after modest strengthening over the past year.

The chart highlights how the currency has traded below its historical average for much of the past several years. For offshore investors funding in stronger currencies, this creates a favourable entry point where income is generated in local terms while potential currency normalisation becomes an additional upside rather than a requirement for return.

In other words, the currency environment does not need to strengthen dramatically to support investment returns, but if it does, it provides an additional tailwind.

Supply Is Contracting

Perhaps the most important structural factor emerging in the New Zealand housing market is the sharp decline in new construction activity.

Following the development boom earlier in the decade, higher financing costs and tighter credit conditions significantly reduced new housing consents across most dwelling categories.

Total new dwelling consents have fallen substantially from the peaks seen in 2021 and 2022. While some recovery occurred during 2025, overall development activity remains materially below prior highs.

Historically, New Zealand property cycles tend to stabilise when supply contracts rather than when demand surges. Reduced development pipelines limit future housing availability, allowing rental markets to firm before capital values begin recovering.

In practical terms, this means the next phase of the property cycle is likely to be driven more by structural supply dynamics than speculative demand.

Taken together, these dynamics suggest that New Zealand is moving into a phase of macro stabilisation rather than rapid expansion.

Monetary tightening has largely passed through the system. Borrowing costs are now near neutral levels. Currency positioning remains supportive for international investors, and new housing supply has slowed significantly.

For investors focused on income-producing real assets, this environment tends to favour properties where demand is anchored in structural drivers such as population growth, education hubs, and urban housing constraints.

Rather than relying on short-term market momentum, our strategy continues to focus on assets with durable rental demand and long-term supply constraints. In periods of financial system adjustment, capital often shifts toward tangible income streams where returns are driven by occupancy and cash flow rather than leverage or speculative pricing.

New Zealand’s institutional stability, transparent legal framework, and structurally constrained housing supply continue to support that positioning.

As global financial infrastructure evolves and capital flows adapt to changing monetary conditions, real assets grounded in measurable economic demand remain a core component of resilient investment portfolios.

Malaysia: Policy Stability, Currency Momentum, and Structural Demand

While New Zealand’s property outlook is increasingly defined by monetary stabilisation and constrained housing supply, Malaysia presents a different but equally relevant investment dynamic. The Malaysian market combines moderate inflation, supportive monetary policy, strengthening currency conditions, and steady real asset demand driven by regional economic integration.

These factors together create an environment where property returns are increasingly anchored in operating cash flow rather than speculative capital appreciation.

Inflation Has Stabilised at Low Levels

One of the most notable macro developments in Malaysia over the past two years has been the stabilisation of inflation.

After peaking during the global inflation surge in 2022–2023, consumer price pressures have steadily moderated. Current projections suggest inflation will remain within the low-to-mid 1–2 percent range through 2026 , reflecting relatively stable domestic demand and controlled cost pressures.

A moderate inflation environment is particularly important for real asset markets. When inflation is stable rather than volatile, both borrowing costs and rental pricing dynamics become more predictable. For property investors, this reduces macro uncertainty and allows income streams to be assessed with greater clarity.

Monetary Policy Remains Supportive

Malaysia’s monetary policy stance has also shifted toward stability.

Following earlier tightening cycles, Bank Negara Malaysia reduced the Overnight Policy Rate from 3.0 percent to 2.75 percent in 2025, signalling that inflation risks had largely been contained while maintaining positive real yields within the financial system.

Unlike more aggressive monetary cycles seen in some developed markets, Malaysia’s rate path has been relatively measured. This moderation has helped support domestic credit conditions while avoiding the sharp disruptions to property financing experienced in some other jurisdictions.

For investors, this policy stability matters. Emerging market risk is often less about interest rate levels and more about policy volatility. Malaysia’s relatively predictable monetary environment provides an important foundation for long-term capital allocation.

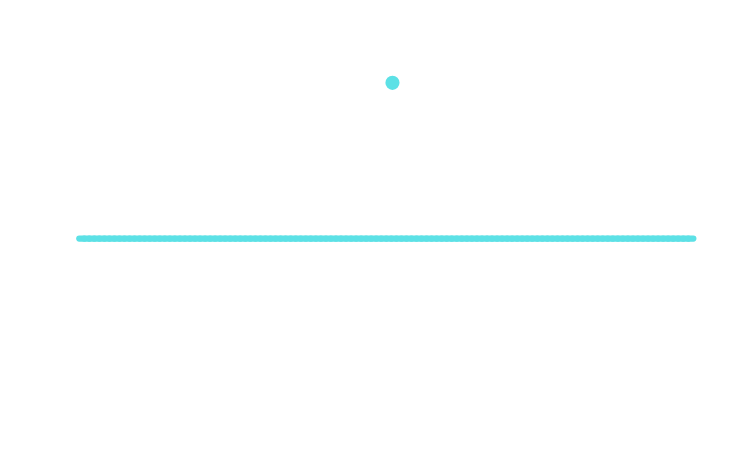

Currency Dynamics Are Shifting

Currency positioning is another important factor shaping investor behaviour.

Over the past decade, the Malaysian ringgit experienced periods of weakness driven by global capital flows and commodity market cycles. However, more recently the currency has strengthened relative to prior lows.

The chart illustrates how the ringgit has moved above its longer-term average against the U.S. dollar after several years of undervaluation.

For international investors, this shift alters the risk profile of Malaysian assets. Currency exposure, which previously required compensation through higher yields, is increasingly becoming neutral or even supportive. When income is generated locally while currency volatility declines, the overall investment equation becomes significantly more attractive.

Periods of financial transition often shift investor focus from broad market narratives toward practical asset allocation. While macro forces shape the environment in which capital moves, investment outcomes ultimately depend on the quality and resilience of individual assets.

With this context in mind, the following section highlights a selection of live property opportunities within markets where structural demand, policy stability, and income visibility continue to support long-term investment positioning.

8. Featured Listings: The Strategic Middle Ground

Perhaps the most important structural factor emerging in the New Zealand housing market is the sharp decline in new construction activity.

Following the development boom earlier in the decade, higher financing costs and tighter credit conditions significantly reduced new housing consents across most dwelling categories.

New Zealand

Tauranga - Multi-Unit Residential

Property Type: Residential Apartment Complex

Estimated Value: ~NZD 40 million

Estimated Yield: ~6%

Land Area: ~2,600 sqm

Floor Area: ~4,500 sqm

Units: 55 apartments

Notes:

A recently constructed multi-level apartment complex located within Tauranga’s established city-fringe residential precinct. The development comprises 55 contemporary apartments held under individual unit titles, providing flexibility for potential staged sell-down strategies while continuing to generate consolidated rental income.

Investment Potential:

Tauranga remains one of New Zealand’s fastest-growing regional centres, supported by strong domestic migration and ongoing infrastructure development. The property’s proximity to the city centre and tertiary education facilities also creates sustained demand from professionals and postgraduate students. The combination of diversified rental income and potential future unit sell-down provides multiple avenues for long-term value creation.

Auckland - Healthcare Commercial Asset

Property Type: Medical / Healthcare Facility

Estimated Investment Value: ~NZD 30 million

Estimated Yield: ~6%

Land Area: 6,048 sqm

Floor Area: 3,149 sqm

Notes :

A purpose-built healthcare facility positioned within one of Auckland’s rapidly expanding suburban corridors. The asset hosts a wide range of medical services serving the surrounding residential population and benefits from strong building quality and extensive onsite parking.

Investment Potential:

Healthcare assets benefit from resilient tenant demand due to the essential nature of medical services. The property’s large site and flexible floor configuration may also allow future repositioning into complementary healthcare uses such as specialist clinics, childcare services, or community health facilities, subject to planning approvals and tenant strategy. These alternative uses could further enhance rental income potential over time.

Waikato - Regional Commercial Asset

Property Type: Commercial / Industrial

Estimated Investment Value: ~NZD 8.5 million

Estimated Yield: ~8%

Land Area: 1,011 sqm

Floor Area: 1,609 sqm

Notes:

A commercial property located within the South Waikato economic corridor supporting industrial and operational tenants. The property benefits from a strong building-to-land utilisation ratio and commercial zoning that supports a range of tenant uses.

Investment Potential:

Regional commercial markets often deliver higher income yields than metropolitan centres due to lower entry pricing and strong demand from local industries. Economic activity across the central North Island continues to be supported by forestry, logistics, and manufacturing sectors, providing stable operational demand for commercial premises in the region.

Malaysia

Subang Jaya - Corporate Office Tower

Property Type: Grade A Corporate Office Tower

Estimated Investment Value: ~RM 120 million

Estimated Yield: ~6%

Floor Area: ~126,000 sq ft

Tenure: Freehold

Notes:

A boutique Grade A office tower located within an established commercial business park in the Subang–Shah Alam corridor. The asset forms part of a mature mixed-use development comprising multiple office towers and supporting retail amenities designed to serve multinational corporations and technology-driven enterprises.

The property benefits from strong regional connectivity via major highways including the Federal Highway, NKVE, and KESAS, while also offering convenient public transport access through nearby LRT and KTM rail links.

Investment Potential:

Office developments along the Subang fringe have historically maintained resilient demand due to their strategic location between Kuala Lumpur’s CBD and the major industrial hubs of Shah Alam and Klang. As corporations continue to decentralise operations away from the congested city centre, well-connected suburban Grade A offices have become increasingly attractive.

The tower’s MSC Malaysia Cybercentre designation further expands the tenant pool by attracting technology firms and multinational companies seeking digital infrastructure and regulatory incentives. Combined with limited new Grade A supply in the immediate corridor, the asset offers potential for stable tenancy and long-term capital appreciation.

Iskandar Puteri - Industrial Manufacturing Facility

Property Type: Detached Industrial Factory with Office

Estimated Investment Value: ~RM 55 million

Estimated Yield: ~7%

Land Area: ~150,447 sqft

Floor Area: ~109,179 sqft

Ceiling Height: ~9 metres

Power Supply: ~1,000 Amp

Notes:

A large-scale detached industrial facility located within the Southern Industrial and Logistics Cluster (SiLC) in Iskandar Puteri. The property comprises a single-storey factory building integrated with a two-storey office component designed to support manufacturing, warehousing, and logistics operations.

Investment Potential:

Iskandar Puteri has emerged as one of Malaysia’s most important industrial investment corridors due to its proximity to Singapore and its role within the Johor–Singapore economic corridor. Industrial assets in the region benefit from strong demand from export-oriented manufacturing, logistics operators, and regional supply chains.

Facilities offering large floor plates, high power capacity, and modern industrial specifications are particularly attractive to manufacturing tenants seeking operational efficiency. As cross-border trade and industrial activity continue to expand across Johor, strategically located industrial properties are well positioned to benefit from sustained tenant demand and rental growth.

Johor Bahru - Commercial Shop Offices

Property Type: Commercial Shop Offices

Estimated Investment Value: ~RM 15 million

Estimated Yield: ~6%

Land Area (per unit): ~143 sqm

Built-up Area (per unit): ~228 sqm

Potential Portfolio Size: ~10 units

Notes:

A portfolio acquisition opportunity within a newly completed commercial shop office development located in one of Johor’s rapidly expanding commercial corridors. The development comprises modern two- to three-storey shop offices designed to support retail, food and beverage, and professional service businesses serving the surrounding residential catchment.

Strategically located within an established township with direct access to the North–South Expressway and proximity to Senai International Airport, the development benefits from strong connectivity to Johor Bahru and the wider Johor–Singapore economic region.

Investment Potential:

Commercial shop offices in established townships benefit from consistent demand generated by nearby residential communities and local business activity. Located within the growing Johor economic corridor and supported by strong highway connectivity, the asset offers potential for stable rental income with long-term growth as commercial activity across the region continues to expand.

Want to discuss any of these opportunities further? Reach out to our team directly:

Contact Information :

Petrus Yen - Managing Director

Petrus@fairhavenproperty.co.nz

Daarshan Kunasegaran

Daarshan.Kunasegaran@fairhavenproperty.co.nz

Disclaimer:

The property details, financial figures, and projections provided in this article are based on publicly available information and internal estimates. They are intended for informational purposes only and do not constitute financial advice or an offer to invest. Projections such as IRR and equity multiples are indicative only and subject to change based on market conditions, financing terms, and execution strategy. Interested parties should conduct independent due diligence and consult with a qualified advisor before making any investment decisions. Fairhaven Property Group accepts no liability for decisions made based on the information presented herein.